For many teachers in Kenya, loans are no longer optional but an essential part of financial planning—whether it’s building a home, paying school fees, starting a side hustle, or handling unexpected expenses. The two most common sources of credit are Sacco loans and bank loans. But the big question in 2025 remains: Which option is better for teachers under today’s economic realities?

This comprehensive guide compares Sacco and bank loans, highlighting their pros, cons, and suitability for teachers. It also ties into broader financial issues like allowances, digital income opportunities, and new reforms affecting educators, to help you make a smarter borrowing decision this year.

Why Teachers Borrow More Than Other Professions

Teachers are some of the most reliable borrowers in Kenya. With the Teachers Service Commission (TSC) payroll system (T-Pay), both Saccos and banks consider teachers low-risk clients since loan deductions are automatically processed from their payslips. This guarantee has made teachers attractive to financial institutions for decades.

But not all borrowing is equal. The choice between Sacco and bank loans directly affects how much you pay in interest, how quickly you access funds, and whether your borrowing contributes to long-term financial growth or just short-term relief.

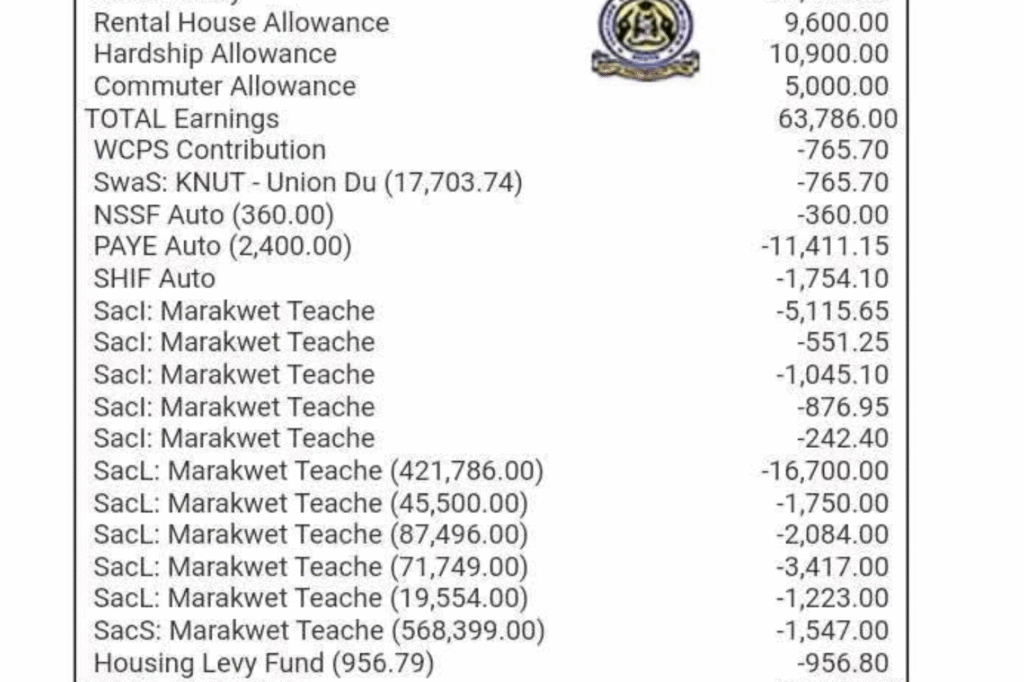

For example, while teacher allowances in 2025 (see TSC Teachers Allowances by Job Groups) have slightly improved income stability, inflation and new deductions on payslips (as highlighted in KUPPET’s protest against new TSC deductions) are pushing many educators into more borrowing than before.

This makes it even more important to understand whether a Sacco or a bank will give you better value for your money in 2025.

Sacco Loans in 2025

Pros of Sacco Loans

- Lower Interest Rates – Most teacher-based Saccos charge between 12%–14% (flat rate), often cheaper upfront than banks.

- Flexible Collateral – Salary and Sacco shares act as collateral, eliminating the need for title deeds or logbooks.

- Mandatory Savings – Every loan boosts your Sacco savings, building long-term financial security and wealth.

- Ownership & Dividends – Since members are shareholders, part of the interest teachers pay comes back as annual dividends.

Cons of Sacco Loans

- Share Boosting Costs – If your shares are low, the Sacco may “top up” your account at your expense before approving the loan.

- Flat Rate Interest – Loans are calculated on the original amount, making them more expensive in the long run.

- Slower Processing – It may take 2–4 weeks to access your money, especially if guarantors are needed.

- Hidden Deductions – Processing fees, insurance, and transaction charges reduce the net disbursed amount.

Bank Loans in 2025

Pros of Bank Loans

- Reducing Balance Interest – You pay interest on the reducing balance, which can make repayment cheaper over time.

- Faster Processing – Loans can be processed in 3–7 days, especially with TSC check-off agreements.

- Higher Loan Limits – Banks often lend larger amounts than Saccos, especially for mortgages or big projects.

- Variety of Products – Teachers can access personal loans, car financing, mortgages, and salary advances.

Cons of Bank Loans

- Stricter Collateral – Some banks demand security like land titles or require strict guarantors.

- Higher Interest Rates – Banks typically charge 13%–16% on reducing balance, which can still be costly.

- Less Community Support – Unlike Saccos, banks don’t grow your savings or give dividends.

- Extra Charges – Facility fees, appraisal charges, and penalties for late payments make loans more expensive.

Comparison Table: Sacco vs Bank Loans in 2025

| Feature | Sacco Loan | Bank Loan |

|---|---|---|

| Interest Rate | 12–14% (flat) | 13–16% (reducing balance) |

| Processing Speed | 2–4 weeks | 3–7 days |

| Collateral | Shares & payslip | Payslip + securities (sometimes) |

| Loan Limit | 3x–4x savings | Based on payslip affordability |

| Hidden Costs | Share boosting, fees | Facility & appraisal fees |

| Repayment Period | Up to 96 months | Up to 72 months (varies) |

| Extra Benefits | Dividends, savings growth | Wide variety of products |

Which is Better for Teachers in 2025?

The right choice depends on your financial goals.

Choose a Sacco loan if you value community-based borrowing, want to build long-term savings, and can afford to wait for processing. Saccos are excellent for medium to long-term needs like school fees, land purchases, or construction projects.

Choose a bank loan if you need fast access to larger amounts and want reducing-balance repayments that lower your interest over time. Banks are ideal for emergencies, mortgages, and car loans.

Smart teachers are even combining the two: saving with a Sacco while using banks for quick, large financing.

Financial Pro Tips for Teachers

- Always request a repayment schedule before signing any loan contract.

- Compare the total cost of borrowing, not just the loan amount.

- Avoid unnecessarily long repayment periods—shorter terms save you interest.

- Keep loans within one-third of your net salary to stay financially healthy.

- Diversify: save with a Sacco, borrow from a bank when urgent, and consider digital side incomes to ease debt pressure.

For example, many teachers are now creating alternative revenue streams online. Platforms like those in Best Online Platforms for Teachers’ Income 2025 show how educators can earn beyond the payslip. Others are adopting AI tools for teachers in 2025 to save time and create more value that can translate into side income.

Borrow Smart, Teach Smart

Borrowing is not just about survival—it can be a tool for growth if done wisely. Teachers must align loans with their bigger financial goals, whether it’s investing in real estate, educating children, or building a side hustle.

The principle of “borrow smart, teach smart,” as discussed in Borrow Smart, Teach Smart, encourages educators to avoid reckless debt and instead use loans strategically to unlock future stability.

This means treating every Sacco or bank loan not as free money, but as an investment decision.

Conclusion

In 2025, teachers should not just ask, “Where can I borrow?” but instead, “Which borrowing choice secures my financial future?” Both Sacco and bank loans have their unique benefits and shortcomings.

If you want long-term financial empowerment, Sacco loans help you save as you borrow. If you want speed and flexibility, bank loans give you bigger amounts faster. The smartest teachers in Kenya will balance both—while also seeking alternative incomes and smart money habits to reduce dependence on loans altogether.

With rising costs, delayed promotions, and increased deductions on payslips, teachers need to think beyond just borrowing. The future belongs to teachers who combine Sacco savings, bank financing, and side hustles powered by digital platforms and AI.