For many Kenyan teachers, joining a Savings and Credit Cooperative Society (SACCO) feels like the safest financial move. SACCOs have a long-standing reputation for being more flexible and affordable compared to commercial banks. They promise lower interest rates, less collateral, and a culture of savings that helps members secure their future. For teachers, SACCO membership is particularly attractive because deductions are made directly from the Teachers Service Commission (TSC) payroll, ensuring convenience and accountability.

But behind the glossy benefits of SACCOs lies a surprising reality. Many teachers are shocked to discover that the actual repayment amount for their loans is far higher than what they initially borrowed. This leaves many questioning whether SACCO loans are truly as affordable as they seem. In this article, we’ll break down the hidden costs, explore real-life teacher experiences, and provide practical tips for making informed borrowing decisions.

The Allure of SACCO Loans

Teachers flock to SACCOs because they offer advantages that banks often cannot match. Among the key benefits are:

- Minimal collateral requirements, usually tied to your payslip.

- Lower advertised interest rates compared to commercial banks.

- Mandatory shareholding, which builds savings alongside borrowing.

- Tailor-made products for teachers, with deductions directly from the T-Pay system.

This combination makes SACCOs feel like the safest bet for teachers looking to borrow. Yet, beneath these advantages are structural conditions and charges that often go unnoticed until it’s too late.

Why Teachers End Up Paying More

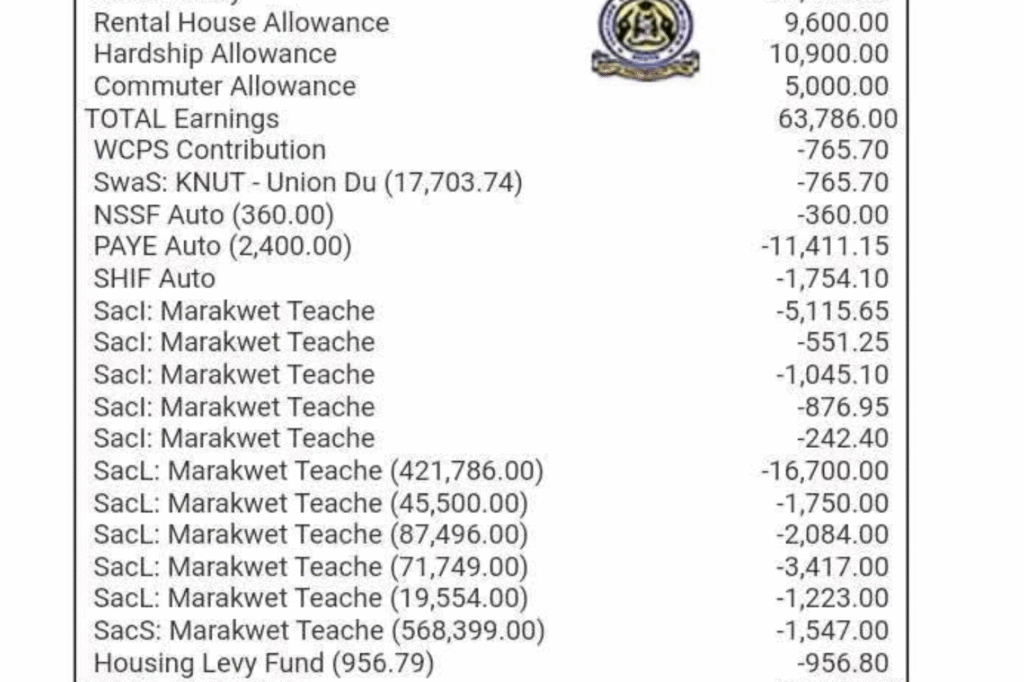

1. Share Boosting Requirements

Most SACCOs demand that members hold shares proportional to the loan they are applying for. For example, a teacher who wants to borrow Ksh 600,000 but only has Ksh 40,000 in shares might be required to “boost” their shares. In some cases, the SACCO adds as much as Ksh 77,500 to the loan to top up the shares.

This boosted amount increases the loan obligation. So instead of repaying just Ksh 600,000, the teacher repays both the loan and the boosted shares, inflating the repayment figure far beyond the actual cash received.

2. Loan Processing and Insurance Fees

Processing fees, usually between 1–3% of the loan, are deducted upfront. Additionally, SACCOs charge insurance fees to cover the loan in case of death or permanent disability. Other transaction charges, such as Ksh 1,000 deducted during disbursement, further reduce the net amount disbursed to teachers. While each fee seems small individually, together they significantly eat into the amount received.

3. Long Repayment Periods

To make loans more “affordable,” SACCOs stretch repayment periods to as long as 96 months (8 years). While the monthly installment looks manageable, the long tenure drastically increases the total interest paid.

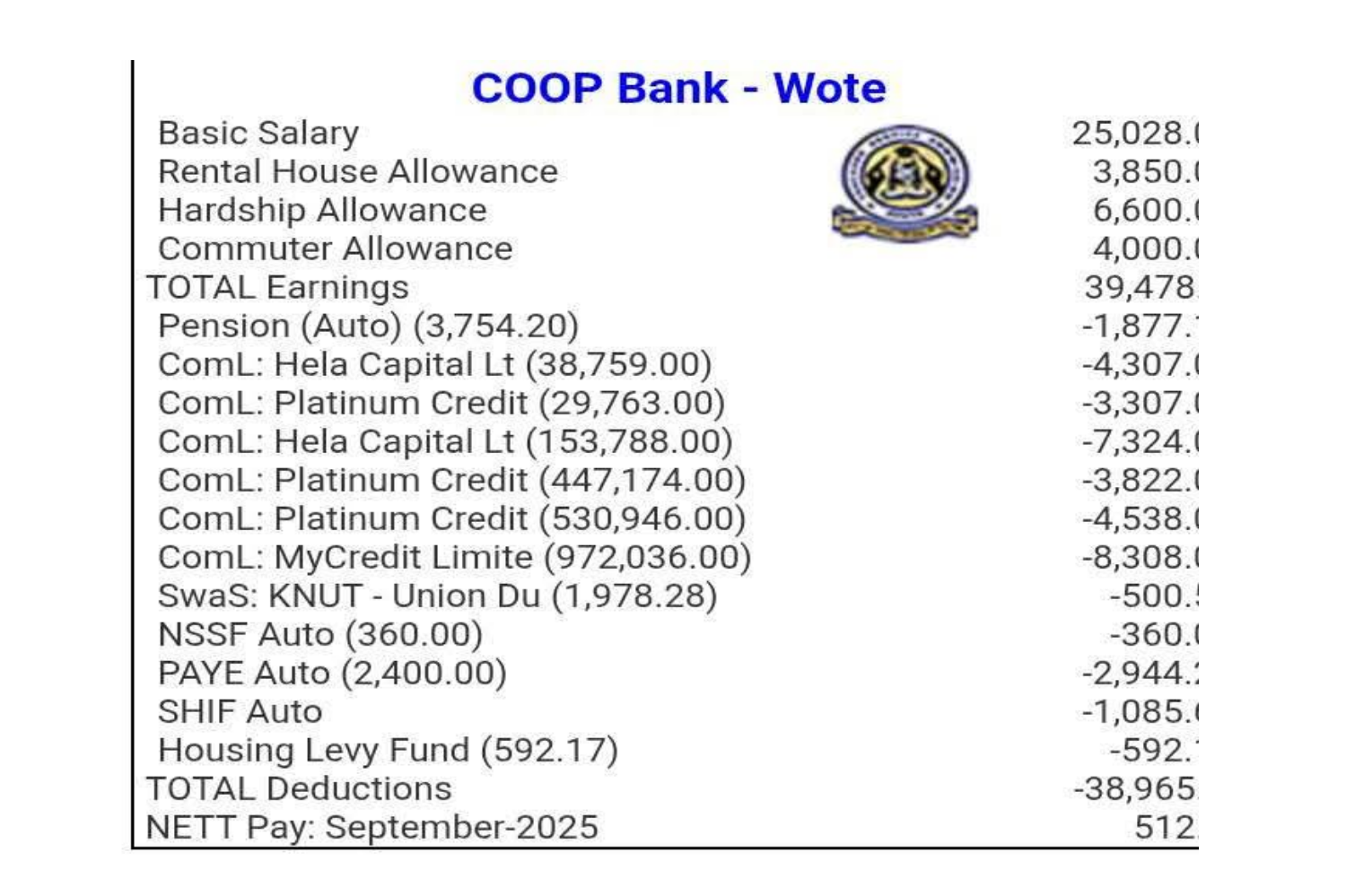

Take this real example:

- Loan Approved: Ksh 1,254,528

- Amount received: Ksh 599,000

- Monthly installment: Ksh 13,068

- Repayment period: 93 months

In the end, the teacher repays more than double the borrowed cash, thanks to boosted shares, interest, and charges.

4. Flat vs. Reducing Balance Interest

Another hidden cost lies in how interest is calculated. Some SACCOs use the flat rate method, where interest is charged on the original loan amount for the entire repayment period. This contrasts with the reducing balance method, used by many banks, where interest is charged only on the remaining balance. Loans calculated on a flat rate basis are far more expensive.

5. Compulsory Savings and Shares

Every time you borrow, SACCOs may increase your compulsory savings and shareholding. While this builds your long-term equity in the SACCO, it reduces your immediate take-home cash. For teachers living on fixed payslips, this can feel like an additional burden.

A Real Case Study: A Teacher’s Experience

One teacher narrated their ordeal:

“I applied for a loan of Ksh 600,000. The SACCO told me to write Ksh 705,000 because my shares were too low. After processing, TSC sent me a message showing Ksh 1,254,528 approved, with a monthly repayment of Ksh 13,068 for 93 months. In the end, I only received Ksh 599,000 in cash after all deductions.”

This case shows the gap between the loan on paper and the reality in your bank account.

What Teachers Should Do Before Taking SACCO Loans

- Request a detailed repayment schedule before committing.

- Ask for the actual net disbursed amount after all deductions.

- Understand how share boosting will affect your repayments.

- Compare SACCO loans with bank loans—especially reducing balance options.

- Avoid extremely long repayment periods, as they lead to higher total interest.

- Consult financial advisors or experienced colleagues before signing.

Alternatives to SACCO Loans

While SACCOs remain popular, teachers should explore other financial avenues:

- Banks: Some banks offer reducing balance loans that can be cheaper over time.

- Mobile loans & microfinance institutions: Useful for small amounts, though interest rates vary.

- Chamas (Investment groups): Often provide interest-free or low-interest loans for members.

- Side hustles & passive income: Teachers can reduce reliance on loans by creating multiple income streams.

You can explore our article on the best online platforms for teachers to earn extra income in 2025.

Financial Awareness and Teacher Welfare

The problem of costly SACCO loans is part of a bigger conversation about teacher welfare in Kenya. Teachers are constantly battling with financial strain, from loan deductions to rising living costs. For example, recent debates have focused on teachers’ allowances and job group disparities in 2025. Understanding SACCO loans is just one piece of the puzzle, as teachers continue to demand fairer financial and professional treatment.

Similarly, digital transformation is opening opportunities for teachers to learn and grow financially. Teachers are increasingly turning to digital solutions—such as the top 5 AI tools every Kenyan teacher should start using in 2025—to supplement their teaching and boost efficiency. These innovations can free up time and resources, reducing overreliance on loans.

The Role of Unions and Advocacy

Teachers’ unions such as KUPPET and KNUT play a vital role in raising awareness about financial issues. Recently, KUPPET SWAL teachers staged protests over new TSC payslip deductions. These protests highlight the frustrations educators face when financial policies tighten their already stretched budgets.

By voicing concerns over SACCO loans, allowances, and deductions, unions are pushing for reforms that will improve teacher welfare.

Conclusion

SACCOs remain a cornerstone of financial security for many Kenyan teachers, but it’s essential to understand that what you borrow is often not what you end up with in your account. Share boosting, hidden fees, long repayment periods, and flat-rate interest calculations inflate the true cost of borrowing.

Teachers must approach SACCO loans with open eyes, asking the right questions and comparing alternatives before signing up. By combining financial awareness with additional income strategies, educators can take control of their finances and avoid falling into hidden debt traps.